Quarterly Report for Premium Condominiums in Tokyo | 2Q FY 2024

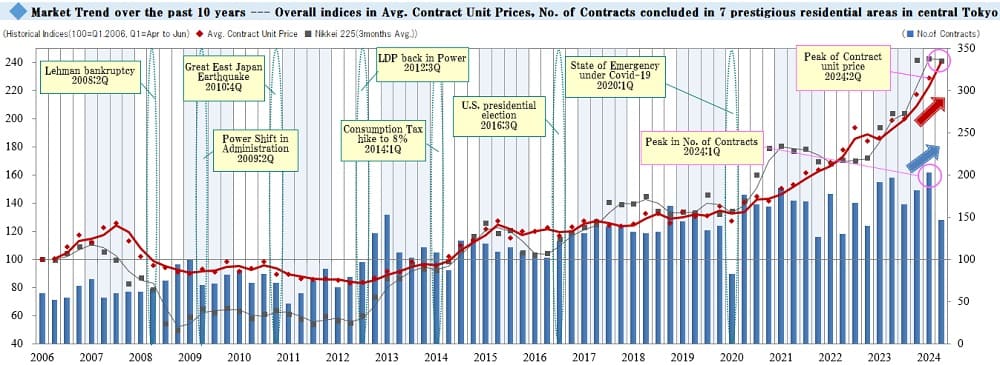

【Chart 1】

This graph shows an index of changes in average contract price per tsubo (*Notes: 1. Indexation using average contract price per tsubo in 1Q / FY 2006 as 100. 2. Tsubo is a Japanese traditional unit of area equal to approx. 3.31sqm.) and the number of contracts concluded every quarter for premium condo. units in 7 prestigious areas of central Tokyo.

Major economic events and Nikkei Stock Average are also shown for reference. The bar graph represents the number of contracts concluded each quarter. The red-line shows a movement in the index of average contract price per tsubo, while the gray-line shows one in the Nikkei stock average.

Based on the overall trend in premium condominiums (above), in the quarter reviewed here (2024: 2Q), the index of the average contract price per tsubo for premium condominium units sold rose by +22.7 points QoQ to 251.6, setting a new record since the beginning of data collection for five consecutive quarters. At the same time, the number of contracts made was down sharply by 56 QoQ to 147, falling below 150 contracts for the first time since 2022: 4Q, six quarters ago.

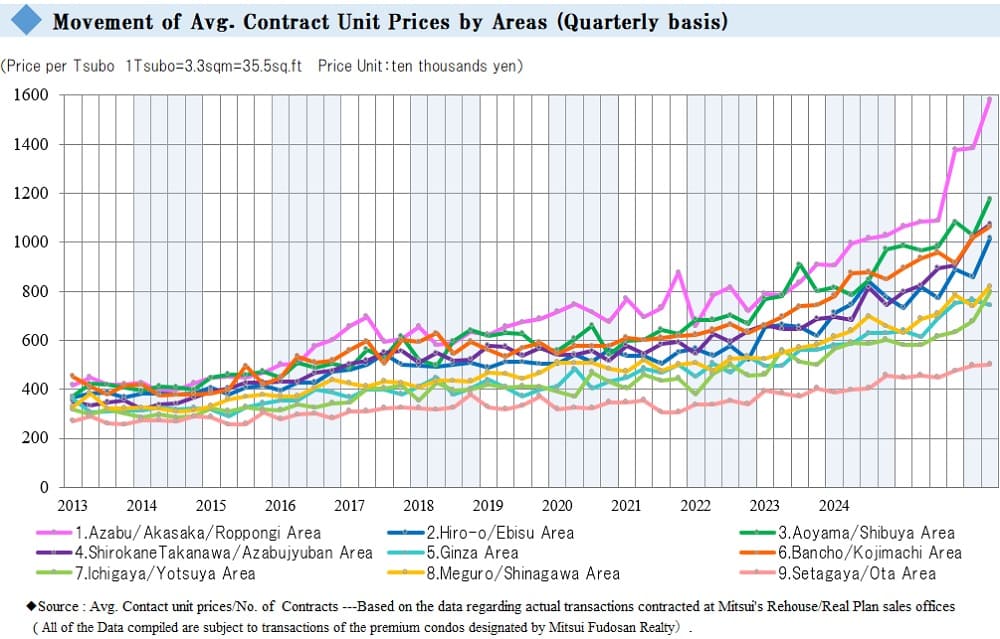

【Chart 2】

The chart above shows the trend in the average contract price per tsubo by area. There were increases in all eight areas other than the “Ginza Area” where the average contract price decreased this quarter. Each of the eight areas went up to a record historical high since the beginning of data collection. Among these, the “Ichigaya / Yotsuya Area” reached a new record high for the fourth consecutive quarter, while the “Shirogane Takanawa / Azabujuban Area” and the “Azabu / Akasaka / Roppongi Area” did so for the fifth and ninth consecutive quarters, respectively.

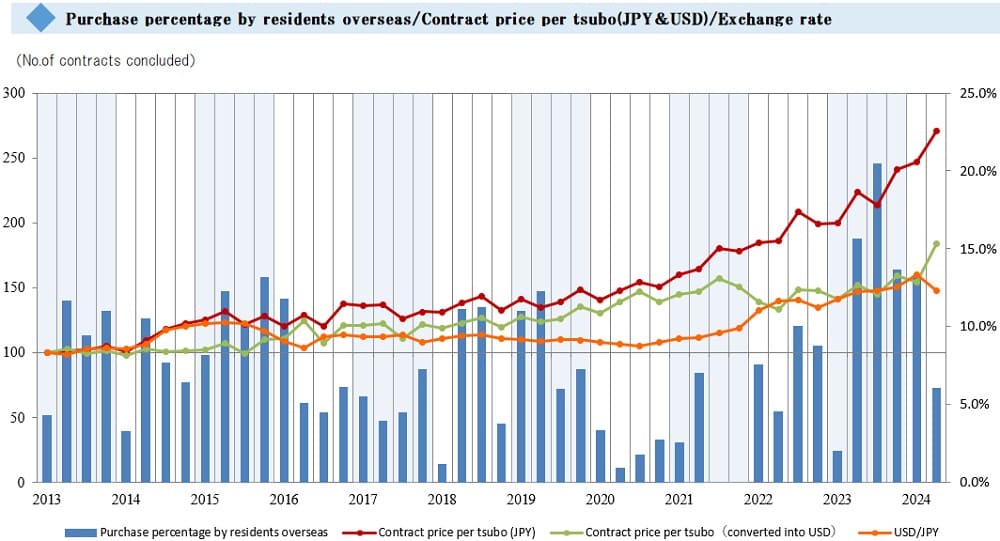

【Chart 3】

The chart above shows the percentage of purchases by overseas residents among Mitsui Fudosan Realty Group transactions and their average contract prices per tsubo (JPY and USD) compared to the exchange rates. The percentage of purchases by overseas residents fell sharply by 7.2 ppt QoQ in this quarter, to 6.1%. The average price per tsubo in this quarter (converted to USD) was up sharply by $11,541 QoQ to $72,496. This is the highest USD price per tsubo since the beginning of data collection, an indicator of the effect of the recent increase in the value of the yen.

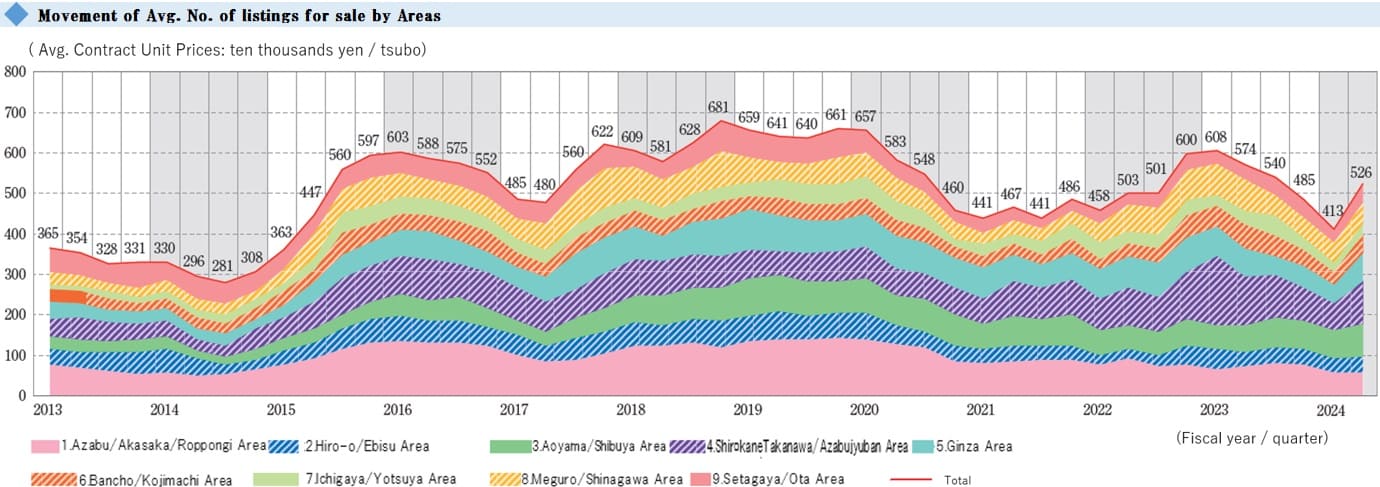

Even as the number of contracts decreased this quarter, the average price per tsubo set a new record high for the fifth consecutive quarter. The inventory for all nine areas combined as of the end of this quarter was 526, up sharply by 27% QoQ. It will be worthwhile to note how this inventory will affect the number of contracts and the average price per tsubo in the ensuing quarters. It will be prudent to keep a close watch on the market impact of large-scale developments planned for completion soon along with trends in the Nikkei Average, exchange rates, and inbound demand in the coming quarters.

【Chart 4】

At the end of the quarter reviewed here (2024: 2Q), inventory for all nine areas stood at 526, down 14 units (2.5%) from the end of the same period last year (2023: 2Q) but up sharply by 113 units (27.3%) from the end of the previous quarter (2024: 1Q). This is the first increase since 2023: 1Q, five quarters ago. A look at performance by area shows increases in all nine areas. The increases were particularly large in the “Ginza Area” (up 25 units, or 54%) and the “Shirogane Takanawa / Azabujuban Area” (up 40 units, or 60%). These two areas especially drove the growth in inventory across all areas.

お問い合わせ Contact us

まずは、お気軽にご相談ください。