Quarterly Report for Premium Condominiums in Tokyo | 1Q FY 2023

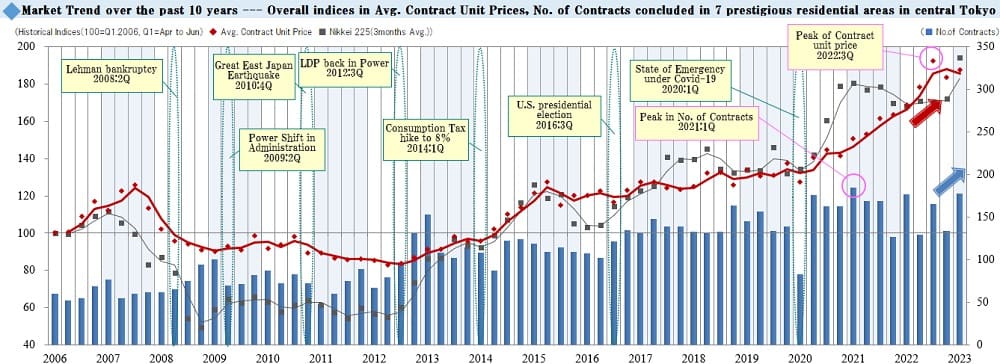

【Chart 1】

This graph shows an index of changes in average contract price per tsubo (*Notes: 1. Indexation using average contract price per tsubo in 1Q / FY 2006 as 100. 2. Tsubo is a Japanese traditional unit of area equal to approx. 3.31sqm.) and the number of contracts concluded every quarter for premium condo. units in 7 prestigious areas of central Tokyo.

Major economic events and Nikkei Stock Average are also shown for reference. The bar graph represents the number of contracts concluded each quarter. The red-line shows a movement in the index of average contract price per tsubo, while the gray-line shows one in the Nikkei stock average.

In the 1st quarter reviewed here (April 1 thru June 30, 2023, based on Japanese fiscal year), the index of average contract price per tsubo for premium condominium units sold changed its direction and rose by 3.5 points QoQ to 187.7, a level to almost reach an all-time high recorded in the 3rd quarter, 2022, since the beginning of data collection. The number of contracts concluded climbed significantly by 40 QoQ to 178, also the second highest level after the record high of the 1st quarter, 2021.

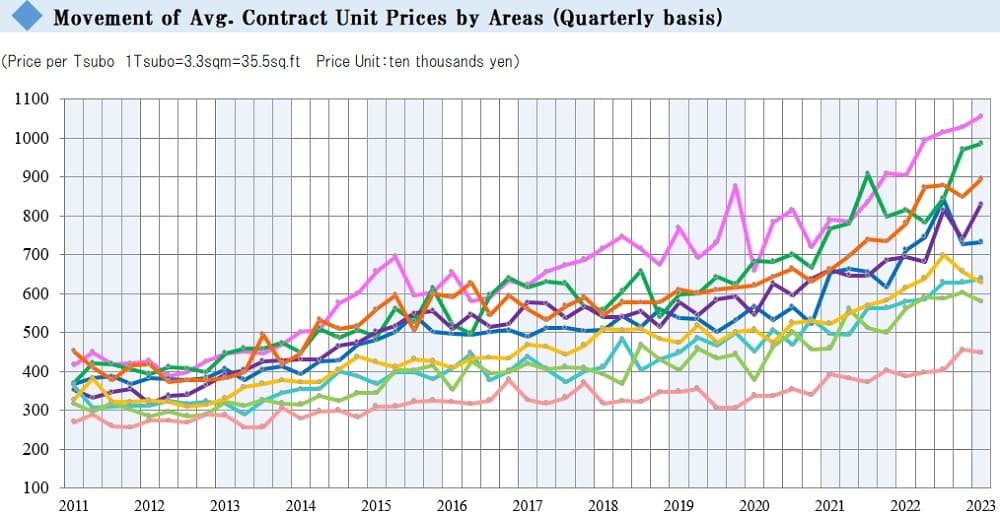

【Chart 2】

The chart above shows average contract price per tsubo. There was a decline in the following four areas, “Hiro-o / Daikanyama / Ebisu Area,” “Ichigaya / Yotsuya Area,” “Meguro / Shinagawa Area,” and “Setagaya / Ohta Area.” On the other hand, the average contract price per tsubo went up to record historical highs since the beginning of data collection in the following five areas, “Azabu / Akasaka / Roppongi Area,” “Aoyama / Shibuya Area,” “Shirogane Takanawa / Azabu-jyuban Area,” “Ginza Area,” and “Bancho / Kojimachi Area.” Especially in the cases of “Aoyama / Shibuya Area,” and “Azabu / Akasaka / Roppongi Area,” this was the second and fourth consecutive time to hit the record high, respectively.

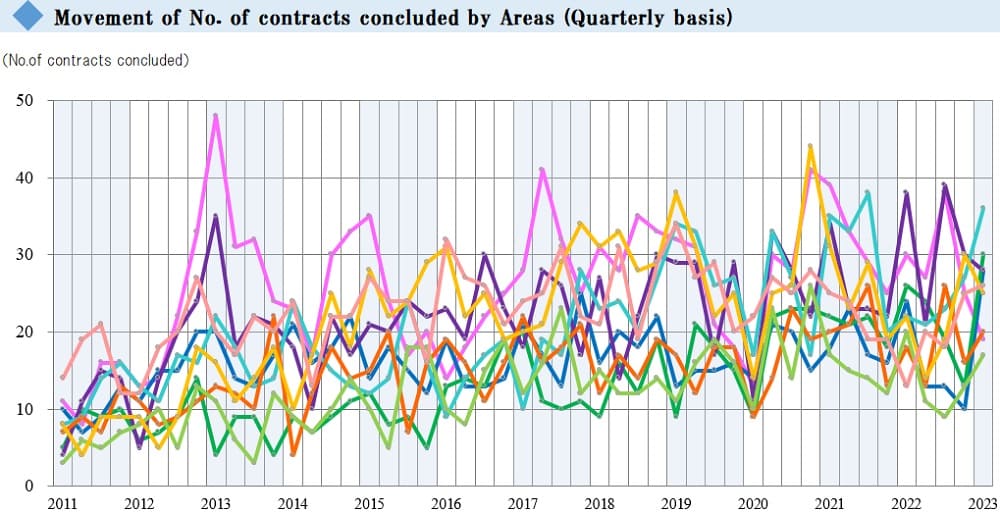

【Chart 3】

Now let's look at the chart above for number of contracts concluded. While the number declined in three areas, i.e. “Azabu / Akasaka / Roppongi Area,” “Shirogane Takanawa / Azabu-jyuban Area,” and "Meguro / Shinagawa Area," it went up in six other areas of “Hiro-o / Daikanyama / Ebisu Area,” “Aoyama / Shibuya Area,” “Ginza Area,” “Bancho / Kojimachi Area,” “Ichigaya / Yotsuya Area,” and “Setagaya / Ohta Area.” Among all, it increased significantly by more than 10 to record an all-time high in “Hiro-o / Daikanyama / Ebisu Area,” and “Aoyama / Shibuya Area.”

In summary, the overall market was robust with an upturn in the index of average contract price per tsubo and a big increase in the number of contracts concluded. However, the inventory for all the nine areas combined as of the end of this quarter was high at 593, decreasing little QoQ from 600, compared to a level a year or two ago (or 485 a year earlier). It will be worthwhile to note how such a large inventory will affect the number of contracts and average price per tsubo in the ensuing quarters.

It will be prudent to keep closely watching impact from large-scale developments and inbound demand, on top of the economic and financial situations.

お問い合わせ Contact us

まずは、お気軽にご相談ください。